Montana requires SR-22 filing for 3 years after a DUI, but the filing itself only mandates liability minimums—not full coverage. Most drivers can drop collision and comprehensive the day SR-22 is filed and save $80–$140/month without violating state compliance.

Does Montana SR-22 Filing Require You to Keep Full Coverage After a DUI?

No. Montana's SR-22 filing requirement obligates you to maintain liability coverage at state minimums—$25,000 per person for bodily injury, $50,000 per accident for bodily injury, and $20,000 for property damage—but it does not mandate collision or comprehensive coverage. Full coverage is a lender or lease requirement, not a state SR-22 requirement.

The confusion stems from the fact that most drivers with auto loans or leases are contractually required to carry collision and comprehensive. But if you own your vehicle outright, you can drop both the moment your SR-22 filing becomes active and still satisfy Montana's DUI compliance obligations. Your SR-22 certificate tracks your liability coverage, not your physical damage protection.

If your vehicle is financed or leased, your lender agreement—not the state—prohibits you from dropping full coverage. Dropping it without lender permission triggers a force-placed insurance policy from your lender at 2 to 3 times the cost of a standard policy, and it often includes a lapse notification to the Montana Motor Vehicle Division that can reset your SR-22 filing period to zero.

How Much You Can Save by Dropping to Liability-Only SR-22 in Montana

Dropping collision and comprehensive on a post-DUI SR-22 policy in Montana typically saves $80 to $140 per month, depending on your vehicle's value, your age, and your county. A 35-year-old driver in Missoula County with a DUI and a 2015 sedan might pay $210/month for full coverage SR-22 but only $85/month for liability-only SR-22—a $125 monthly reduction.

The savings increase if your vehicle is older or higher-mileage. Collision and comprehensive premiums are calculated as a percentage of your vehicle's actual cash value. A 2010 pickup truck with 140,000 miles might only justify $30/month in combined physical damage premiums on a clean record, but after a DUI that same coverage can cost $90–$110/month in the non-standard market.

Most non-standard carriers in Montana—Bristol West, Dairyland, The General, GAINSCO—price liability-only SR-22 policies more aggressively than full coverage policies because their risk exposure is capped at your liability limits. If you own your vehicle outright and it's worth less than $5,000, dropping to liability-only is almost always the correct financial decision during your 3-year filing period.

Find out exactly how long SR-22 is required in your state

What Happens to Your SR-22 Filing if You Drop Collision and Comprehensive

Nothing. Your SR-22 filing remains active and compliant as long as your liability coverage stays continuous at Montana's minimum required limits. The SR-22 form—filed by your carrier with the Montana Motor Vehicle Division—certifies that you carry liability insurance, not that you carry full coverage.

When you drop collision and comprehensive, your carrier does not file a cancellation notice with the state. Only a full policy cancellation, non-renewal, or lapse in liability coverage triggers an SR-22 termination notice to the MVD. Changing your coverage levels within an active policy is a policy endorsement, not a filing event.

Your 3-year SR-22 filing clock continues uninterrupted. Montana calculates your filing period from your conviction date or reinstatement date, depending on whether your license was suspended. Dropping physical damage coverage does not reset that timeline or extend your compliance obligation.

When You Cannot Legally Drop Full Coverage on an SR-22 Policy

If your vehicle has an outstanding loan or lease, your lender agreement requires you to maintain collision and comprehensive coverage with specific deductible limits—typically $500 or $1,000 maximum. This is a private contract obligation between you and your lender, not a state insurance requirement, but violating it has severe consequences.

Dropping full coverage without lender consent triggers a force-placed insurance clause in your loan agreement. Your lender will purchase a collateral protection policy on your behalf and add the premium—often $1,200 to $2,400 annually—to your loan balance. Force-placed policies cover only the lender's financial interest in the vehicle, not your liability or your own injuries, and they do not satisfy Montana's SR-22 filing requirement because they do not include liability coverage.

If you drop full coverage and your lender force-places a policy, your original SR-22 liability policy may lapse if you stop paying it, triggering an SR-22 cancellation notice to the Montana MVD. That lapse resets your 3-year filing period to zero and subjects you to a new license suspension until you refile. The only way to drop full coverage on a financed vehicle is to pay off the loan or refinance it as an unsecured personal loan, eliminating the lender's collateral interest.

How to Drop Full Coverage Without Triggering a Filing Lapse

Contact your carrier before making any coverage changes and confirm that dropping collision and comprehensive will not cancel your policy. Most non-standard carriers allow mid-term endorsements to reduce coverage, but a few require you to wait until your policy renewal date to avoid triggering a full policy rewrite.

Request a revised declarations page showing your new liability-only coverage limits and confirming that your SR-22 filing remains active. This document is your proof that your filing is still valid if the Montana MVD later questions your compliance. Keep a copy in your vehicle and a digital copy accessible on your phone.

Verify that your new monthly premium reflects the removal of collision and comprehensive. If your premium decreases by less than $60/month, your carrier may not have processed the endorsement correctly, or your vehicle's physical damage premiums were already minimal. Non-standard carriers sometimes bundle collision into liability pricing for low-value vehicles, making the savings negligible.

Should You Keep Full Coverage Even if You Own Your Vehicle Outright?

It depends on your vehicle's replacement value and your ability to absorb a total loss. If your vehicle is worth $8,000 or more and losing it would prevent you from working or meeting your probation obligations, keeping collision and comprehensive—even at post-DUI rates—may be worth the cost.

Most DUI drivers in Montana are managing stacked compliance: SR-22 filing, possible ignition interlock device requirements, DUI education courses, court fees, and restricted license conditions. Losing your vehicle to an at-fault accident or theft during this period can cascade into missed probation check-ins, missed work, and ultimately a probation violation. For drivers in rural Montana counties where public transit is nonexistent, full coverage functions as income protection.

If your vehicle is worth less than $4,000 and you have access to a backup vehicle or reliable transportation alternatives, dropping to liability-only is almost always the correct decision. The 3-year cost of maintaining full coverage on a low-value vehicle in the non-standard market often exceeds the vehicle's replacement value by year two.

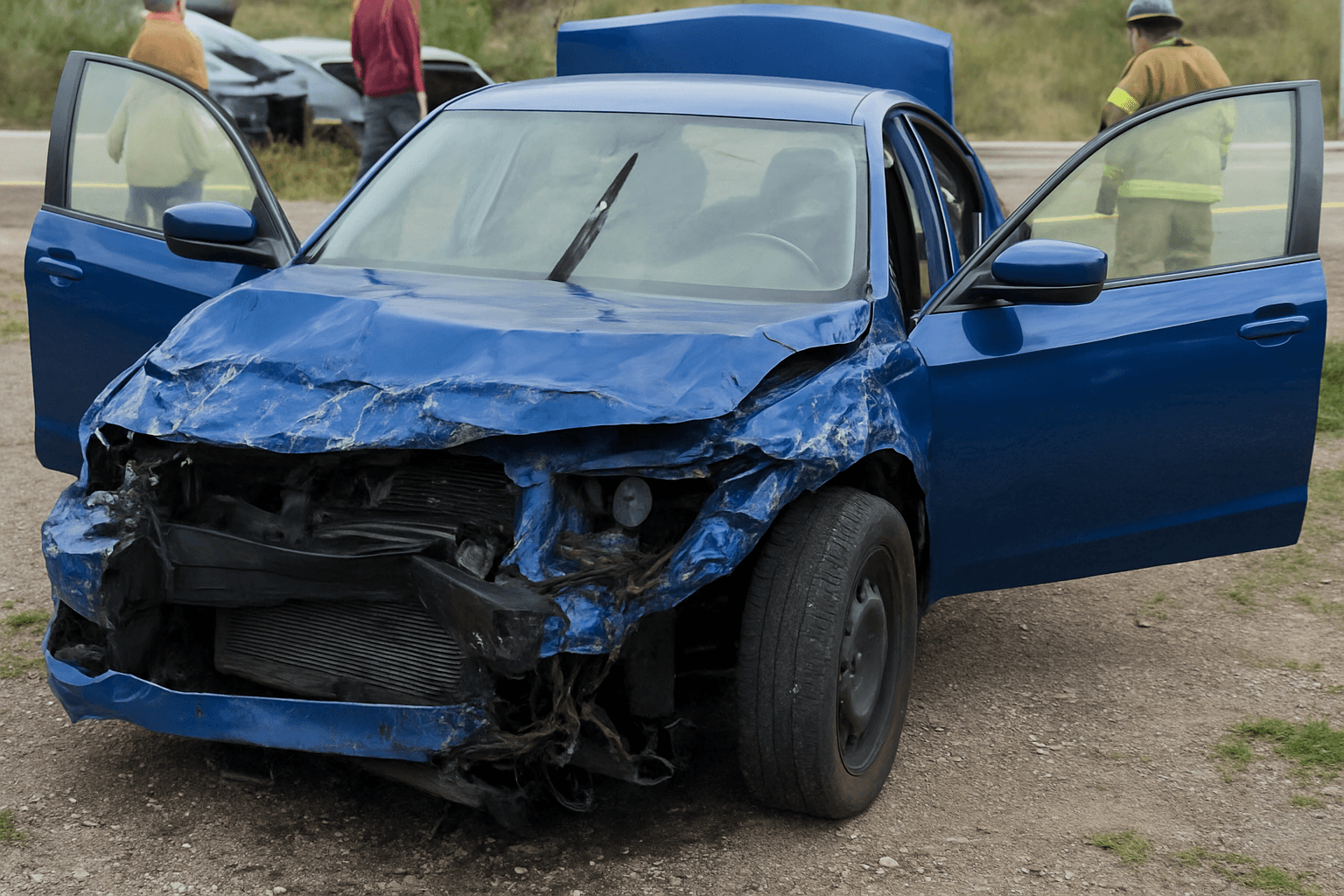

What Happens if You Drop to Liability-Only and Later Total Your Vehicle

You receive nothing from your insurance carrier. Liability-only coverage pays for damage you cause to other people and their property—it does not cover damage to your own vehicle, regardless of fault. If you cause an accident, your liability coverage pays the other driver's repair bills up to your policy limits, but your vehicle repair or replacement cost is your responsibility.

If another driver causes the accident and they carry valid liability insurance, you file a third-party claim against their policy. Montana is a fault-based state, meaning the at-fault driver's liability coverage pays for your vehicle damage. But if the at-fault driver is uninsured or underinsured—and you dropped your uninsured motorist property damage coverage along with collision—you have no coverage for your vehicle loss.

Montana does not require uninsured motorist property damage coverage, only uninsured motorist bodily injury coverage. Many drivers drop UMPD when they drop collision to maximize savings, but this leaves them fully exposed if an uninsured driver totals their vehicle. If you drop to liability-only, keeping UMPD at a $250 deductible typically adds only $8 to $15/month and covers the most common loss scenario in rural counties: hit-and-run or uninsured driver accidents.